By Olufemi Awoyemi

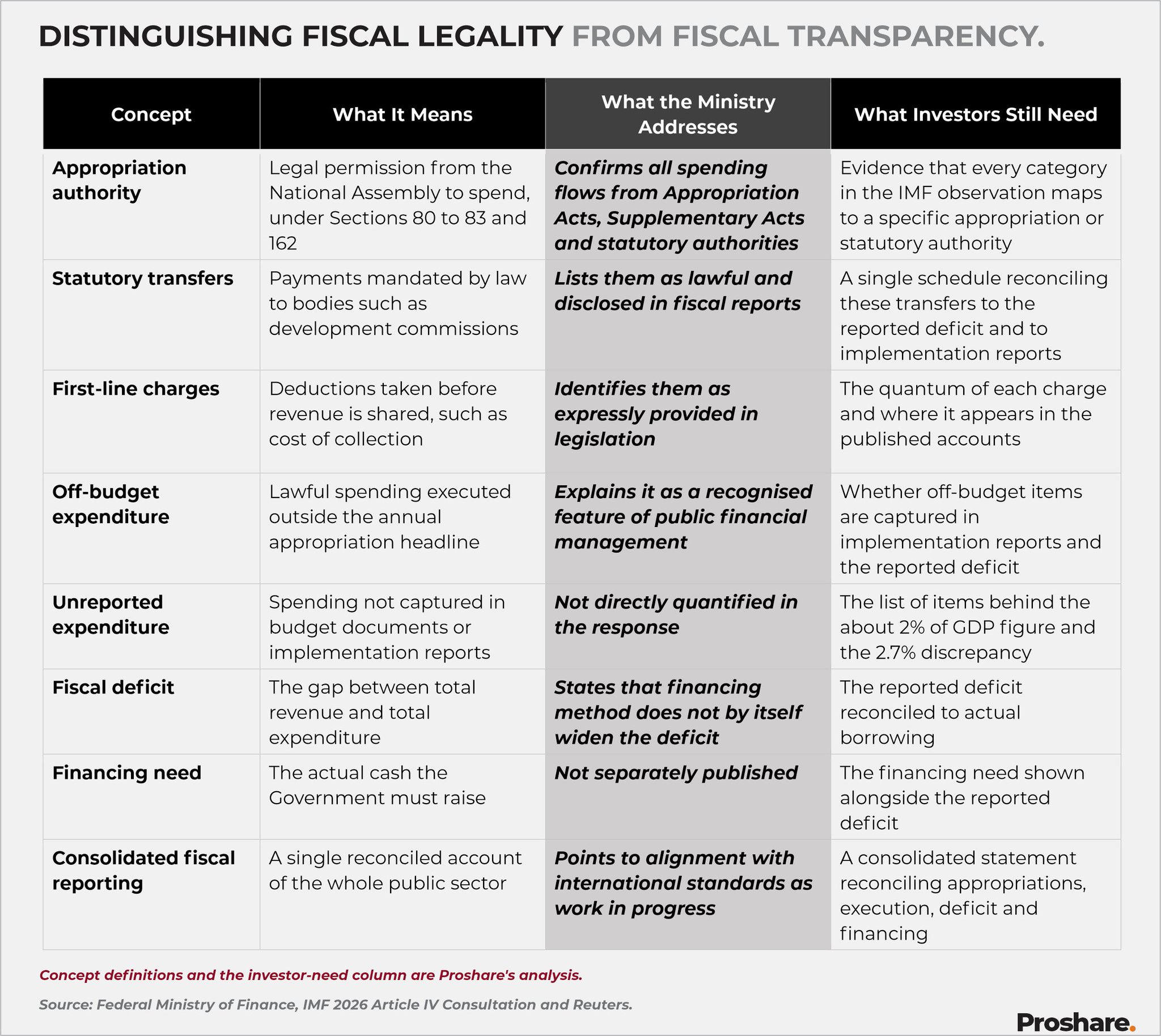

Nigeria is having the wrong argument about the right problem. The Ministry affirms that federal spending is authorised under Sections 80 to 83 and 162 of the 1999 Constitution, and that spending outside the appropriation headline is neither secret nor illegal.

The IMF concern is different in kind. Its 2026 Article IV

Consultation commended three years of stabilising reforms, called for a neutral fiscal stance, and tied an estimated statistical discrepancy of 2.7% of GDP to spending outside the Accountant General’s accounts.

The IMF Resident Representative puts unreported expenditure at about 2% of GDP, and the most-cited naira figure, over approx. N8 trillion, is the Ministry’s own restatement. The reported consolidated deficit rose to 4.4% of GDP in 2025 from 2.4% in 2024.

The accusation the @FinMinNigeria rebuts is not the observation the @IMFNews made. The Fund’s point is about the completeness of the record, not the lawfulness of the spending. Below, we present a table that distinguishes between fiscal legality and fiscal transparency.

Recalling What Executive Order 9 Adds

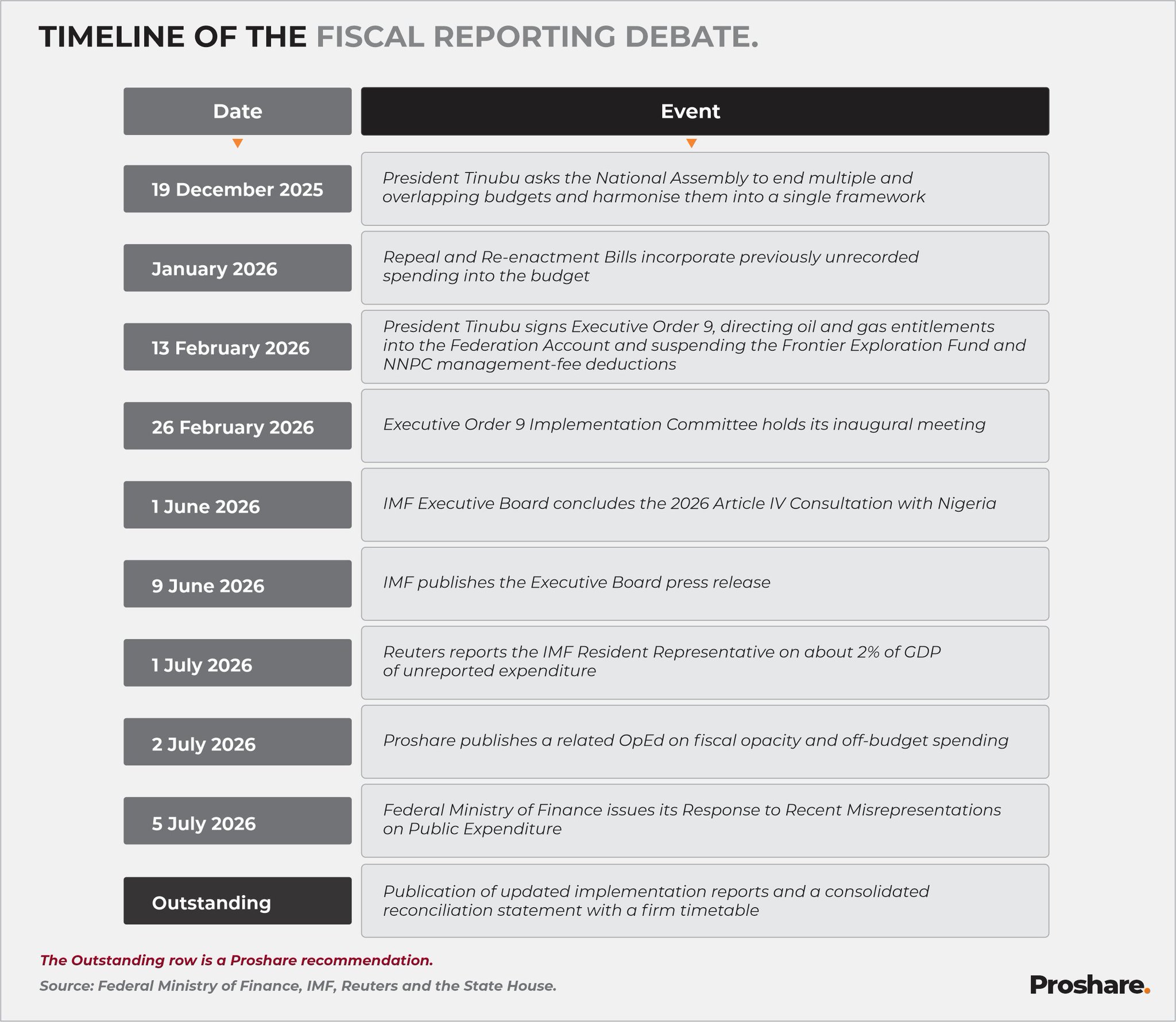

Executive Order 9, signed in February 2026 and anchored on Section 44(3) of the Constitution, is the revenue-side counterpart to this reporting question. It directs royalty oil, tax oil, profit oil and profit gas straight into the Federation Account, suspends the 30% Frontier Exploration Fund and the 30% @nnpclimited management fee, and moves gas-flare penalties out of the Midstream and Downstream Gas Infrastructure Fund.

Officials project that full implementation could add up to N14.57 trillion to distributable revenue. This is the same shift from opacity to legibility the IMF seeks on the expenditure side. Unless the suspended funds and projected inflows are captured in the reconciled accounts, and the durability of statutory change by executive instrument is settled, the Executive Order risks seeding a fresh discrepancy as it closes an old one.

What Remains Unresolved and What would settle it

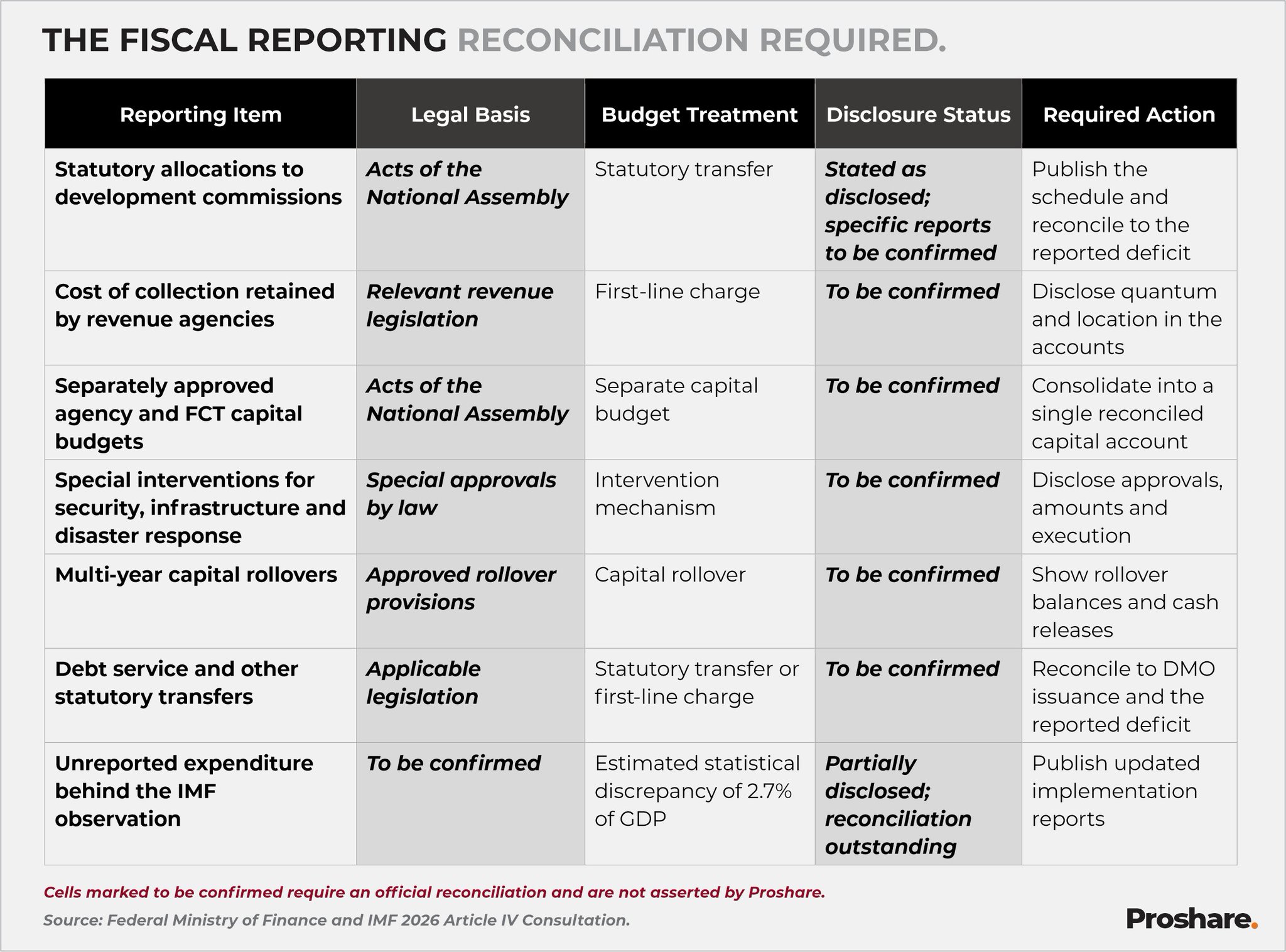

A denial does not close an information gap. What the clarification does not yet provide is a reconciliation. The most confidence-building response available to the Federal Government is a single public reconciliation statement that identifies the expenditure categories underlying the IMF observation, their legal basis, the implementing entities, their treatment in the budget and fiscal reports, their cash and financing treatment, and their effect on the reported deficit.

The market has moved beyond whether the spending was authorised, to whether the published accounts allow a user to reconcile appropriations, implementation reports, the reported deficit, and actual borrowing without a residual gap.

The Government has already accepted the direction of travel. The President asked the National Assembly on 19 December 2025 to end the practice of multiple and overlapping budgets and to harmonise them into a single framework, and the authorities have begun revising budget laws to incorporate previously unrecorded spending. What is outstanding is publication and timing.

This is very important given the President’s long-standing interest in rebuilding institutional credibility by eliminating the opacity of our budget processes and the nation’s financial management of procurement. Table 2 below sets out the reconciliation required.

Why Markets Should Care

A reported deficit that understates the financing need complicates debt sustainability analysis and the pricing of government securities and weakens fiscal and monetary coordination while the Central Bank holds policy tight against inflation of 15.4% year-on-year. Table 3 below sets out the directional risk identified by the EMIU team.

Closing Thoughts and Outlook

The IMF has not asked Nigeria to prove its innocence but to complete its accounts, and President Tinubu’s Executive Order 9 shows the same instinct on the revenue side. A consolidated statement that captures both the expenditure categories and the Order’s revenue effects would convert this moment into a governance gain rather than a standing risk premium.

Proshare interprets this debate as a reporting-quality uncertainty rather than a scandal and separates the three figures in circulation to prevent market participants from being misled by their conflation.

The path forward is a single reconciliation with a timetable, a governance opportunity the Government can convert. This analyst note therefore offers the necessary calibration as a data-led firm for the fiscal-reporting debate, not a promotion of any position.

Awoyemi is the founder of Proshare