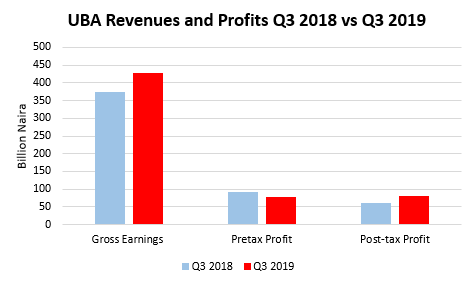

Alabingo Finance Report|United Bank for Africa (UBA) defiled the slow pace of Nigerian economic growth to grow its post-tax by 32 per cent to N81.63 billion in the third quarter of 2019, its financial statement recently sent to the Nigerian Stock Exchange has shown. Its pre-tax profit was up 24.17 per cent to N98.23 billion during this period.

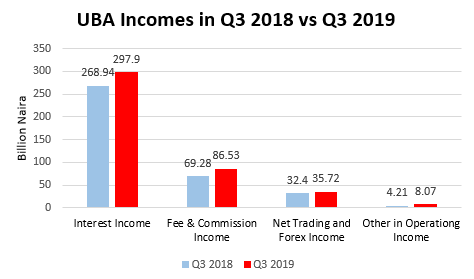

The bank grew gross revenue by 14.23 per cent to N428.74 billion, driven by dividend income, which rose almost 100 per cent, as other operating income jumped 91.46 per cent to N8.07 billion in Q3 2019, compared to N4.21 billion in the comparable last year.

Meanwhile, while interest income increased 10.77 per cent to N297.90 billion, fee and commission income was higher by 24. 90 per cent to N86.53 billion, on the back of 71 per cent rise in Credit-related fees and commissions.

The bank was able to rake in higher net trading and foreign exchange income by 10.24 per cent to N35.72 billion, helped by revenue from fixed income securities, in spite of the restriction by the Central Bank of Nigeria (CBN) of the volume investment commercial lenders could make in the fixed income market in September.

The apex had in September 2019 directed all commercial banks operating in Nigeria to maintain a minimum loan-to-deposit ratio (LDR) of 60 per cent and just a month later, it raised it to 65 per cent, in a bid to a bid to spur economic growth through the real sector.

Mr. Moses Ojo, Head, Research and Business Development, PanAfrican Capitals told our correspondent that the CBN directive has made banks to engage in aggressive deposit mobilization, as stiff competition in the banking sector has made margins to continue to thin out.

The CBN had hinted in May that it would peg the amount of investment commercial lenders can make in government instruments. This may have reflected in UBA investment securities which dipped -12.49 per cent to N1.40 billion in Q3 2019 from N1.60 billion in the same period last year.

While UBA spent 17. 55 per cent more as interest income expenses, amounting to N138.99 billion, it cost N23.24 billion to raise its fees and commission income, which was 27.49 per cent higher than it spent during the same period last year.

The bank had a total Assets of N4.96 trillion, an increase over the N4.87 trillion recorded in December 2018. Customer Deposits also grew to N3.37trillion, while loans and advances increased by 21.99 per cent to N1.99 trillion as its total liabilities upped 10.19 per cent to N4.41 trillion as at September 2019.

Also, shareholders’ fund rose 10.5 per cent to N555.53 billion. Commenting on the results, the Group Managing Director, UBA Plc, Kennedy Uzoka, said: “The resilience of our business model and our focused growth of earning assets have yielded a 10.8 per cent growth in interest income. In addition to the commendable yield on interest-earning assets, we also achieved a 22.1 per cent growth in non-interest income, driven largely by the increased penetration of our superior digital banking offerings, credit expansion, remittances, and other lifestyle transactional services.”

“UBA remains committed to its vision of becoming the undisputed leading and dominant financial services institution in Africa. We will continue to innovate and lead in all our business segments, whilst delivering top-notch operational efficiencies and best-in-class customer service. We are beginning to realise early gains from our ongoing Transformation Program and I am indeed excited about the days ahead,” Uzoka stated.

Also throwing more light on the bank’s financial performance and position, the Group CFO, Ugo Nwaghodoh said “with the results achieved in the quarter under consideration, the bank remains on track to deliver its earnings target for the year. We were able to grow the loan book by 14.7 per cent, (well ahead of our guidance) focusing on growth poles of various economies in which we operate. We have also developed new credit products targeted at specific consumer and SME market segments, and will continue to do so with strict adherence to best credit/underwriting standards, as we strive to achieve the statutory loan-to-funding ratio threshold set by the apex bank.”

Leave a Reply